In September, the International Monetary Fund (IMF) agreed to approve another loan to Pakistan. This time, the approved loan was worth US$7 billion, the second-largest IMF loan taken by the country.

Why do countries go for IMF loans?

The IMF is not a routine lender. It doesn’t provide any project-specific loan assistance but comes forward to help countries hit by financial crises. According to the IMF website, the loans are meant to provide breathing space, while the focus is primarily on policy reforms towards economic stabilization and growth. The IMF says its motto is to promote “sustainable growth and prosperity for all of its member countries.”

IMF loans mandate that recipient countries carry out economic reforms as agreed in the loan agreement. Steps such as expanding the tax base, managing inflation, reducing subsidies, stabilizing the currency, and implementing other structural economic reforms are unavoidable. The IMF releases loan amounts in phases or tranches, and each subsequent release depends on the agreed-upon terms being strictly followed. Failure to comply results in the IMF holding up further releases

IMF loans should be seen as a temporary relief measure to handle the balance-of-payments (BoP) crisis, also called a currency crisis, and not a long-term solution. Countries facing deep economic problems and difficulty paying for their imports or servicing their debt request loan assistance from the IMF to meet the demand and avoid possible economic default.

Special Drawing Right (SDR)

The IMF uses a unique international reserve asset called the Special Drawing Right (SDR). Instead of using a traditional currency, the SDR’s value is derived from a basket of five major currencies: the US dollar, the euro, the Chinese renminbi, the Japanese yen, and the British pound.

As of August 1, 2022, the US dollar holds the largest share in the basket at 43.38%, followed by the euro at 29.31%. The renminbi, yen, and pound account for 12.28%, 7.59%, and 7.44%, respectively. This basket composition is reviewed every five years to reflect the relative importance of currencies in the global economy.

According to the IMF website, one SDR equals approximately US$1.32 as of November 8, 2024.

Pakistan’s journey with the IMF

Facing fiscal problems and economic unpredictability in a newly formed nation, Pakistan approached the IMF to become a member country. The IMF Board of Governors approved its membership application on February 1, 1950, and the country joined the institution on July 11, 1950.

The country’s economic conditions forced it to turn to the lender for the first time in 1958, though that loan was not drawn. Falling export prices, rising inflationary pressure, reduced foreign exchange, and scaled-down development projects were significant problems Pakistan was facing. These problems were a natural byproduct of the prevailing situation in the country. Pakistan, as a newly formed nation, faced troubling times due to an unstable political atmosphere: seven prime ministers in 11 years (from 1947 to 1958), the assassination of the country’s first prime minister in 1951, and the first military coup in 1958.

March 1965 saw the first successful loan transaction with the IMF to bail out the country. The IMF sanctioned loan assistance worth up to US$37.5 million to help the country handle depleting foreign exchange reserves amid a sharp rise in imports. The loan was intended to meet the BoP crisis Pakistan was facing.

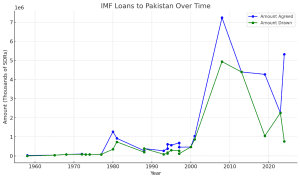

Since then, Pakistan has, on average, requested an IMF loan every 2.5 years.

The 1965 bailout started a series of bailouts that Pakistan is still embroiled in. The trend was driven by factors such as the country’s defeat in the 1965 India-Pakistan war, which led to severe economic troubles, and the 1971 war and the separation of East Pakistan as the independent country of Bangladesh, which deepened the economic crisis and caused further deterioration in efforts to industrialize the country.

Pakistan is the fourth-largest debtor

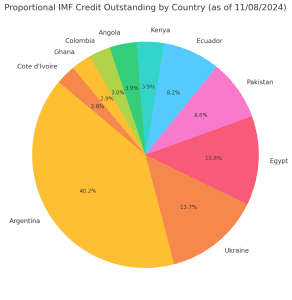

Of the IMF’s top 10 biggest debtors, Argentina has taken over 40% of the total current debt owed to the IMF under its various programs. Based on an SDR to USD comparison, Argentina’s current outstanding debt amounts to approximately US$41 billion. Pakistan, ranking fourth, has an outstanding balance of US$8.8 billion. Ukraine and Egypt rank second and third.

US$34.2 Billion

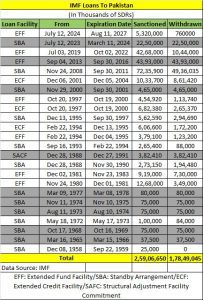

According to the IMF database, loans sanctioned to Pakistan total 25.9 billion SDRs, which, at current exchange rates, comes out to be US$34.2 billion. Of this sanctioned amount, loans worth US$23.56 billion were actually disbursed, indicating Pakistan’s struggle to meet IMF terms on numerous occasions.

Pakistan was able to withdraw 68% of the largest loan sanctioned to it by the IMF, worth US$7.6 billion, in 2008. Of the 23 loans completed so far, Pakistan has only been able to get the complete sanctioned amount nine times, which indicates a policy paralysis approach prevailing in the country. Desperation to control and mitigate the impending economic crisis forces it to rush to the lender, but its internal political and social compulsions mostly prevent it from meeting the norms set in the mutual agreements.

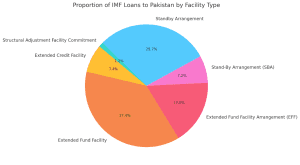

What Different IMF Loan Instruments Say About Pakistan’s Economy

The IMF has a long history of providing financial assistance to countries facing economic challenges, with Pakistan being a prominent example. Over the years, Pakistan has sought the agency’s assistance multiple times through various lending instruments, including the Stand-By Arrangement (SBA) used 13 times; the Extended Fund Facility (EFF) used seven times; the Extended Credit Facility (ECF) used three times; and the Structural Adjustment Facility Commitment, used once.

Established in 1952, the SBA is a critical aid tool for both emerging and advanced economies needing short-term financial assistance. Typically lasting up to three years, the SBA requires borrowing countries to implement reforms targeting the root causes of their economic difficulties. Continued loan disbursement is conditional upon meeting these objectives.

Pakistan’s current economic situation reflects the IMF’s use of the EFF, designed for countries facing BoP crises due to deep-seated structural issues. The EFF offers longer-term support and repayment periods than the SBA, enabling countries to carry out comprehensive reforms to address these underlying challenges.

Seeking relief through the IMF’s EFF comes with a price. The EFF imposes stringent conditions, requiring borrowing countries like Pakistan to undertake significant structural reforms targeting macroeconomic fundamentals such as income generation, revenue collection, tax base expansion, and market liberalization. The IMF also emphasizes policy reforms to address institutional and economic weaknesses. During negotiations for the EFF agreement in July 2019, the IMF explicitly urged Pakistan to curb its defence spending.

The Extended Credit Facility (ECF), another IMF instrument, is aimed at countries facing long-term BoP difficulties. Rooted in the Poverty Reduction and Growth Trust (PRGT) program, the ECF is intended to support low-income countries. However, it demands strict adherence to structural benchmarks, policy adjustments, and quantitative targets, which often limit a government’s spending capacity.

Even earlier IMF interventions, such as the 1988 Structural Adjustment Facility, imposed significant constraints on Pakistan. The country was required to liberalize interest rates, reduce public sector borrowing, reform its banking sector, tackle budget deficits, manage debt levels, control inflation, bolster foreign exchange reserves, and address currency depreciation. The shift from reliance on SBAs to EFFs signals a troubling trend, indicating a decline from an emerging economy to a lower-income nation facing persistent BoP and related problems.

By Santosh Chaubey (DD India)