Nine years after the rollout of the Goods and Services Tax (GST), India’s landmark indirect tax reform has transformed the country’s taxation landscape by replacing a fragmented system of multiple central and state levies with a unified national framework. Introduced on July 1, 2017, under the principle of “One Nation, One Tax,” GST has evolved into one of India’s most significant economic reforms, promoting transparency, strengthening cooperative federalism, improving tax compliance and supporting the formalisation of the economy.

The reform subsumed 17 central and state taxes and 13 cesses into a common tax structure, eliminating the cascading effect of “tax on tax” that had long increased costs for businesses and consumers. By standardising tax rates and procedures across states, GST created a common national market and simplified the movement of goods and services across the country.

Over the past nine years, the tax regime has undergone continuous refinement through policy reforms, digital innovation and close coordination between the Centre and the states. These changes have sought to balance revenue generation with ease of doing business while making the tax system more efficient, transparent and citizen-friendly.

GST is structured as a destination-based consumption tax, meaning revenue accrues to the state where goods or services are ultimately consumed rather than where they are produced. It is levied on the supply of goods and services rather than separately taxing manufacturing, sales and services, thereby creating a more streamlined taxation framework. The system follows a dual model under which the Centre levies Central Goods and Services Tax (CGST), states levy State Goods and Services Tax (SGST) on intra-state transactions, and Integrated Goods and Services Tax (IGST) is applied to inter-state supplies.

The institutional backbone of the reform has been the GST Council, which has emerged as a key platform for cooperative federalism by bringing together the Centre and states to jointly decide tax rates, exemptions and procedural changes. Through regular meetings, the Council has responded to evolving economic needs while ensuring policy consistency across the country.

Supporting this framework is the Goods and Services Tax Network (GSTN), jointly owned by the Centre and state governments, which provides the digital infrastructure for GST administration. The technology-driven platform enables online registration, return filing, tax payments and other compliance-related services, significantly reducing paperwork and improving efficiency.

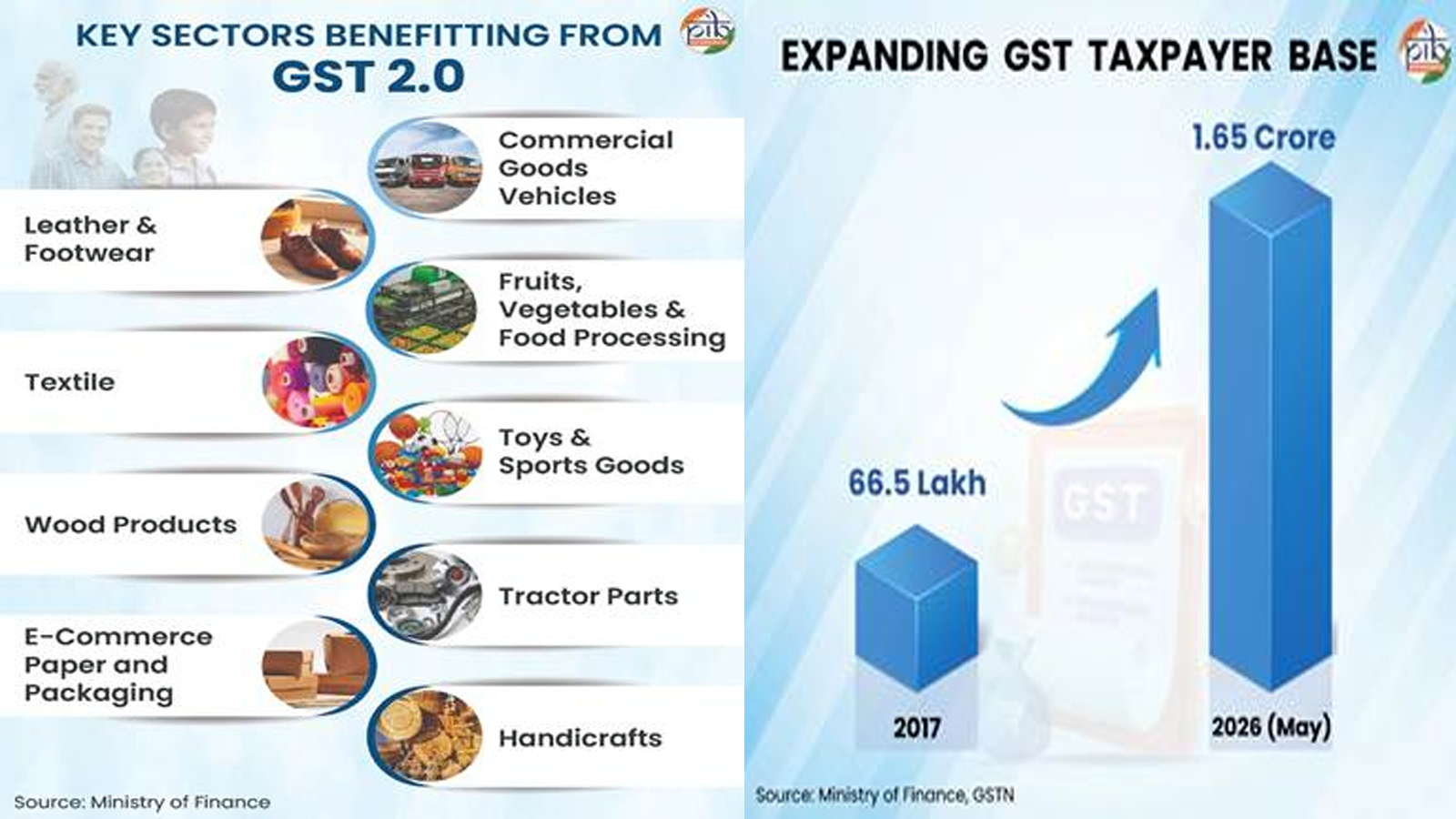

The latest phase of reforms, widely referred to as GST 2.0, came into effect on September 22, 2025, following approval by the 56th meeting of the GST Council. Designed to simplify taxation further while supporting economic growth, the reforms introduced a streamlined rate structure centred primarily around two tax slabs of 5 per cent and 18 per cent.

To maintain revenue neutrality while rationalising the broader tax structure, a separate 40 per cent tax rate was introduced for luxury and sin goods, including tobacco products, aerated beverages, lottery and online gaming, high-end cars, yachts and private aircraft.

The reforms also eased compliance requirements by simplifying registration procedures, return filing and refund mechanisms. The measures have particularly benefited micro, small and medium enterprises (MSMEs), startups and small taxpayers by reducing procedural burdens and lowering compliance costs.

The impact of GST 2.0 extends beyond tax simplification. By lowering costs for businesses and consumers, the reforms are intended to encourage consumption, improve affordability and stimulate economic activity. GST exemptions on insurance products and essential medicines have strengthened household financial security while improving access to healthcare.

Industry has also benefited from reduced tax rates on key inputs and sectors such as cement and handicrafts, lowering production costs and enhancing competitiveness. Simplified tax classifications have reduced disputes over product categorisation, while corrections to inverted duty structures have supported domestic value addition and strengthened India’s export competitiveness.

Over the years, the GST regime has introduced several measures aimed specifically at easing compliance for smaller businesses. The GST registration threshold for suppliers of goods was increased from ₹20 lakh to ₹40 lakh in 2019, while the turnover limit under the Composition Scheme was doubled to ₹1.5 crore for most states, enabling more small businesses to benefit from simplified tax payments and reduced compliance requirements.

The introduction of the Quarterly Return Filing and Monthly Payment (QRMP) scheme in 2020 further eased compliance for taxpayers with annual turnover of up to ₹5 crore by allowing quarterly filing of returns. Small taxpayers with no business transactions have also been allowed to file NIL GST returns through SMS, reducing procedural complexity.

Additional relief has been provided to small businesses selling goods through e-commerce platforms by exempting eligible intra-state suppliers from mandatory GST registration. Low-risk applicants now benefit from an expedited registration process that enables approvals within three working days.

The government has also reduced the pre-deposit amount required for filing GST appeals and introduced waivers of interest and penalties for specified demand notices relating to the financial years 2017-18, 2018-19 and 2019-20, subject to prescribed conditions.

One of the defining features of GST’s evolution has been the increasing reliance on technology and data-driven administration. Digital platforms such as the GSTN portal and e-invoicing have enabled real-time capture of invoice data, reducing manual reporting, improving data accuracy and minimising mismatches in tax filings.

Automation has significantly simplified compliance through pre-filled returns, automated reconciliation and real-time validation of input tax credit claims, reducing errors and procedural requirements for taxpayers.

Advanced technologies, including artificial intelligence, machine learning and data analytics, are now being used to identify tax evasion through risk-based monitoring of registration, scrutiny and compliance patterns. By focusing enforcement efforts on high-risk taxpayers, these technologies have reduced unnecessary regulatory intervention for compliant businesses while improving overall tax administration.

The broader economic impact of these reforms is reflected in India’s GST collections and expanding taxpayer base. The number of registered GST taxpayers has grown from 66.5 lakh in 2017 to 1.65 crore by May 2026, indicating a significant expansion of the formal economy.

GST collections have also witnessed sustained growth over the years. Gross GST collections increased from approximately ₹7.4 lakh crore in 2017-18 to around ₹22.27 lakh crore in 2025-26, compared to nearly ₹13.76 lakh crore in 2021-22. The momentum has continued into the current financial year, with collections touching approximately ₹4.37 lakh crore during April and May 2026.

Rising collections have increasingly become a high-frequency indicator of economic activity, reflecting stronger consumption, expanding trade, improved compliance and a wider taxpayer base. The growing use of technology has also contributed to more predictable revenue collection, supporting fiscal transparency and macroeconomic stability.

As India marks nine years of GST, the reform represents far more than a structural change in taxation. It reflects an evolving system that continues to simplify compliance, strengthen cooperative federalism, encourage formalisation, promote digital governance and improve the ease of doing business. With GST 2.0 building on nearly a decade of reforms, the government sees the tax regime as an important pillar supporting economic growth, inclusive development and the broader vision of Viksit Bharat.