India’s rural economy is witnessing a quiet but significant transformation as expanding access to institutional credit, digital financial services and targeted government policies reshape the way millions of farmers, rural entrepreneurs and households access finance. Once heavily dependent on informal moneylenders, the country’s rural credit system has evolved into a diversified institutional network that supports agriculture, allied sectors, rural enterprises and household needs while strengthening inclusive economic growth.

The transformation reflects decades of institutional reforms backed by technology and financial inclusion initiatives. Institutions such as the National Bank for Agriculture and Rural Development (NABARD), Scheduled Commercial Banks, Regional Rural Banks (RRBs), Cooperative Banks and Small Finance Banks now form the backbone of India’s rural credit ecosystem, delivering timely and affordable finance across the country.

The growing reach of formal finance is reflected in NABARD’s Rural Economic Conditions and Sentiments Survey conducted in May 2026. According to the survey, 77.2 per cent of rural households reported higher consumption levels, indicating improved purchasing power and sustained demand. Access to institutional finance has also expanded considerably, with around 51 per cent of households relying exclusively on formal sources of credit, while more than 27 per cent access both institutional and non-institutional channels.

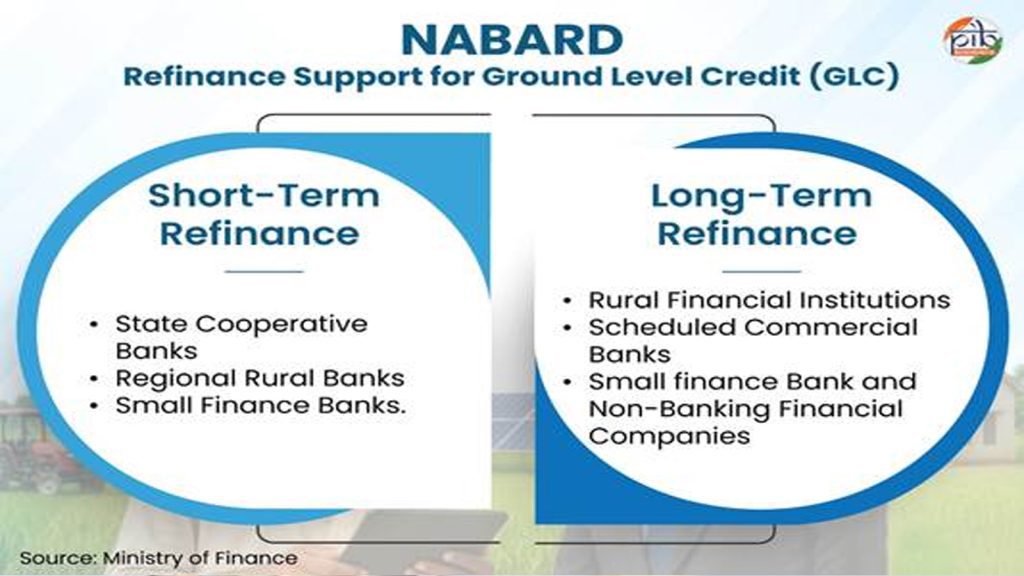

At the centre of India’s rural credit architecture is NABARD, which serves as the apex development financial institution for agriculture and rural development. The institution strengthens rural finance through refinance support, rural infrastructure financing, institutional development and supervision of Cooperative Banks and Regional Rural Banks. It also plays a key role in promoting financial inclusion, preparing district credit plans and supporting government initiatives aimed at expanding access to formal financial services.

India’s rural credit journey has evolved steadily since Independence through a series of landmark policy interventions. The establishment of the National Agricultural Credit (Long-term Operations) Fund and the State Bank of India in 1955 marked the first major push towards expanding rural banking. The nationalisation of 14 major commercial banks in 1969 redirected institutional lending towards priority sectors, particularly small farmers, significantly increasing the flow of credit to rural areas.

The establishment of NABARD in 1982 further strengthened the institutional framework by integrating financing, developmental and supervisory functions for agriculture and rural development. Subsequent initiatives such as the Self-Help Group-Bank Linkage Programme launched in 1992, the Kisan Credit Card (KCC) Scheme introduced in 1998, the Pradhan Mantri Jan Dhan Yojana (PMJDY) launched in 2014, the Pradhan Mantri Mudra Yojana introduced in 2015 and technology-driven platforms such as Jan Samarth and e-KCC since 2022 have progressively expanded financial inclusion and improved credit delivery.

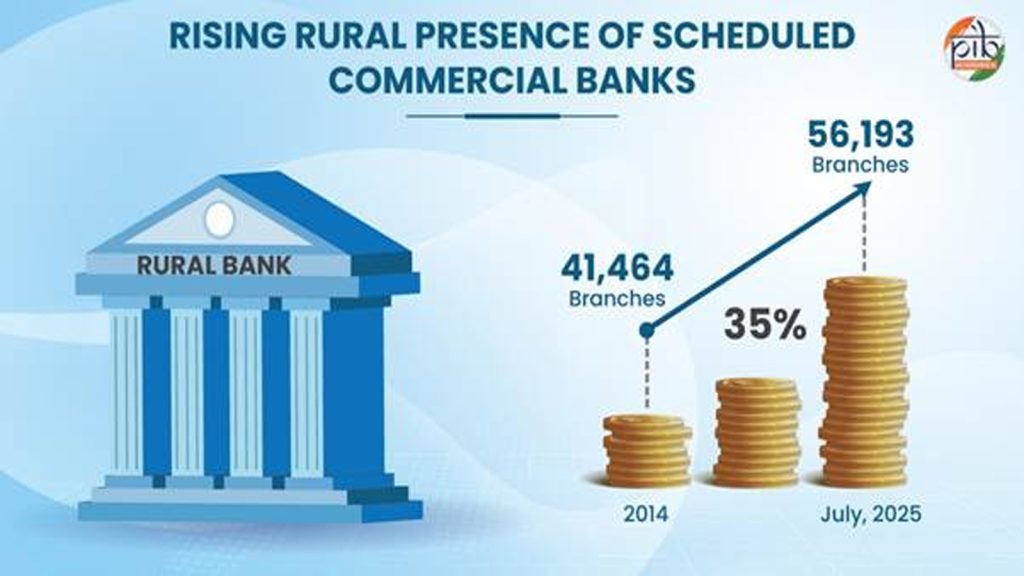

A wide institutional network now supports rural credit across the country. Scheduled Commercial Banks have significantly expanded banking access through physical branches, business correspondents, digital platforms and Direct Benefit Transfer (DBT) initiatives. The number of rural branches of Scheduled Commercial Banks increased from 41,464 in 2014 to 56,193 by July 2025, strengthening the reach of institutional finance. Around 120 Scheduled Commercial Banks are currently providing banking services nationwide.

Regional Rural Banks continue to play a critical role in extending institutional credit to small and marginal farmers, agricultural labourers, artisans and rural entrepreneurs. Established under the Regional Rural Banks Act, 1976, the country now has 28 RRBs operating through more than 22,000 branches across 700 districts.

The cooperative banking system remains another important pillar of rural finance. Its multi-tier structure comprising State Cooperative Banks, District Central Cooperative Banks, Primary Agricultural Credit Societies (PACS), State Cooperative Agriculture and Rural Development Banks and Primary Cooperative Agriculture and Rural Development Banks has played a significant role in expanding banking habits among rural communities. According to RBI and NABARD, the cooperative network currently includes 1,458 Urban Cooperative Banks, 34 State Cooperative Banks and 352 District Central Cooperative Banks.

Small Finance Banks, introduced following the Union Budget 2014-15, have further expanded financial inclusion by focusing on underserved sections of society. Licensed by the Reserve Bank of India, these banks provide credit to small businesses, marginal farmers, micro industries and entities in the unorganised sector through technology-driven operations. Eleven Small Finance Banks are currently operational across the country.

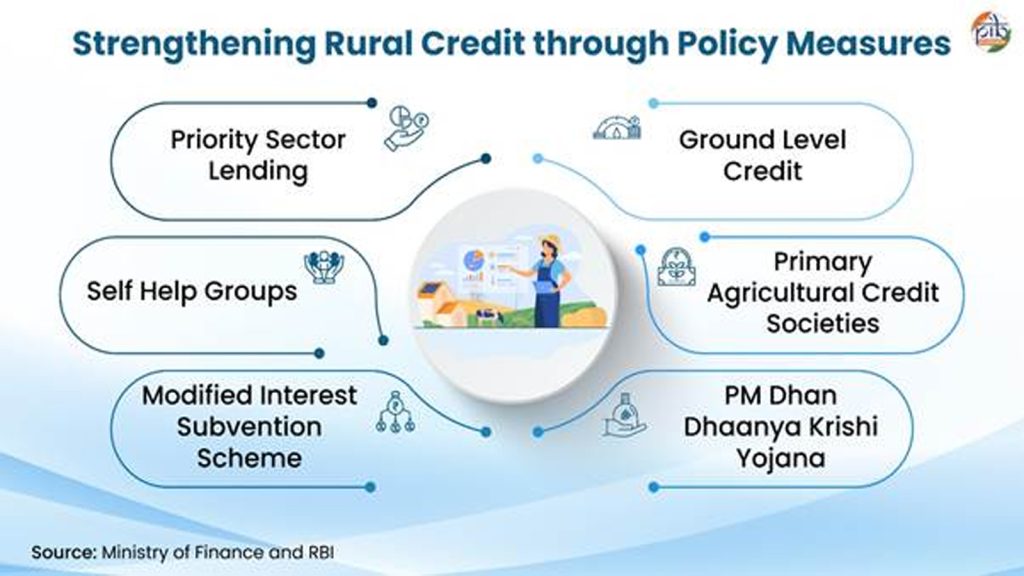

Government policy has also played a crucial role in expanding rural credit. The Priority Sector Lending framework mandates banks to allocate a fixed share of their lending towards agriculture and other underserved sectors. Commercial Banks, Regional Rural Banks, Small Finance Banks and eligible Cooperative Banks are required to earmark at least 18 per cent of their Adjusted Net Bank Credit or Credit Equivalent of Off-Balance Sheet Exposures towards agriculture, with dedicated sub-targets for non-corporate farmers and small and marginal farmers.

Alongside Priority Sector Lending, annual Ground Level Credit (GLC) targets have steadily expanded agricultural finance. For FY 2025-26, the government fixed a record agricultural credit target of ₹32.50 lakh crore, including a dedicated sub-target of ₹5 lakh crore for animal husbandry, dairying and fisheries. The target represents more than a fourfold increase from ₹8 lakh crore in FY 2014-15. During FY15 to FY24, agricultural credit disbursement grew at an annual rate exceeding 13 per cent, supported by NABARD’s refinance assistance to banks.

Women’s financial inclusion has received a significant boost through the Self-Help Group-Bank Linkage Programme initiated by NABARD and strengthened through the Deendayal Antyodaya Yojana-National Rural Livelihoods Mission (DAY-NRLM). By July 2025, more than 10.05 crore rural women had been mobilised into over 90.90 lakh Self-Help Groups across the country.

As of July 10, 2026, over 19.83 lakh Self-Help Groups were operational under DAY-NRLM, with cumulative loan disbursements of ₹13.28 lakh crore since inception. Supporting this ecosystem are Bank Sakhis, who help Self-Help Group members open bank accounts, submit loan applications and ensure timely repayments. Around 50,548 Bank Sakhis have facilitated access to bank credit exceeding ₹12.18 lakh crore since 2013-14.

Primary Agricultural Credit Societies continue to serve as the grassroots foundation of the cooperative credit system. In 2023, the government approved a plan to establish two lakh new multipurpose PACS as well as dairy and fishery cooperative societies across all panchayats over five years. As of January 20, 2026, 32,836 new societies had been registered and 15,793 dairy and fishery cooperatives strengthened. Simultaneously, digitisation efforts are underway, with 61,842 out of 79,630 approved PACS having migrated to a common ERP-based national software platform by March 10, 2026.

Affordable credit remains central to government policy through the Modified Interest Subvention Scheme (MISS), which provides farmers with short-term loans through the Kisan Credit Card at an effective interest rate of as low as four per cent for prompt repayment. The Union Budget 2025-26 expanded the scheme by increasing the loan limit under MISS from ₹3 lakh to ₹5 lakh. The lending limit for fisheries and allied activities was also enhanced to ₹5 lakh, while collateral-free agricultural loans were increased from ₹1.6 lakh to ₹2 lakh per borrower from January 2025.

Another major initiative, the PM Dhan Dhanya Krishi Yojana, approved in July 2025, seeks to accelerate development in 100 low-performing agricultural districts through convergence of 36 Central schemes implemented by 11 ministries. Along with improving agricultural productivity, crop diversification, irrigation and post-harvest infrastructure, the programme aims to strengthen farmers’ access to both short-term and long-term agricultural credit. Based on cumulative output till May 2026, Banka in Bihar, Mahoba in Uttar Pradesh, Charaideo in Assam, Kishanganj in Bihar and Tikamgarh in Madhya Pradesh have emerged as the top-performing districts under the scheme.

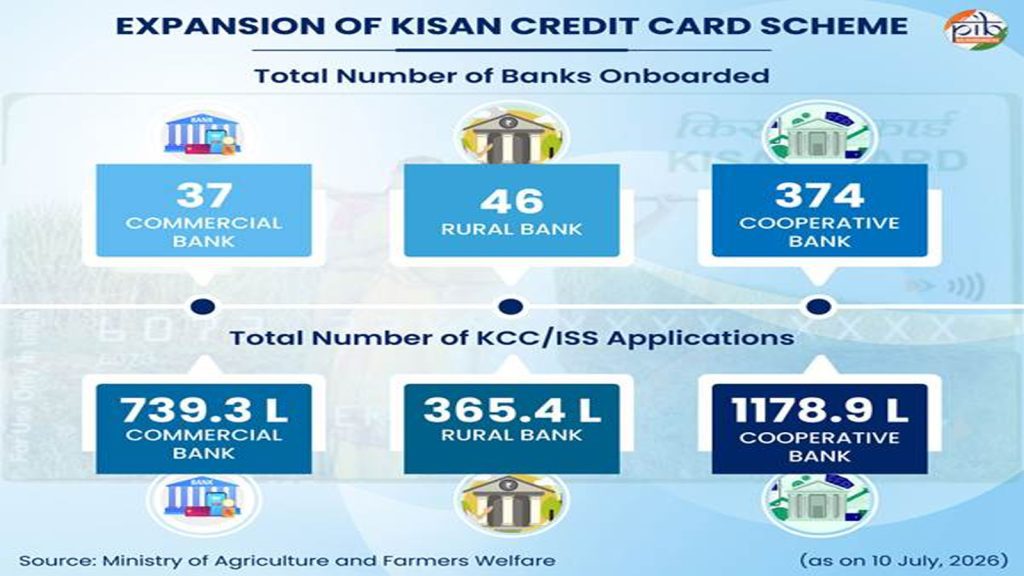

The Kisan Credit Card continues to remain the flagship instrument for providing timely and affordable institutional credit to farmers. It supports financing for crop cultivation, post-harvest activities, marketing expenses, household consumption, farm maintenance and allied agricultural activities. As of July 8, 2026, commercial banks had received nearly 739 lakh KCC applications, Regional Rural Banks over 365 lakh applications and cooperative banks more than 1,178 lakh applications. The scheme now covers owner cultivators, tenant farmers, sharecroppers, oral lessees, Self-Help Groups, Joint Liability Groups and, since 2019, beneficiaries engaged in dairy, fisheries and animal husbandry.

Digitisation has further transformed KCC operations through NABARD’s e-KCC portal, enabling farmers to submit loan applications online or through Common Service Centres without visiting bank branches. The platform has reduced loan processing time to nearly two days, significantly improving ease of access to agricultural credit.

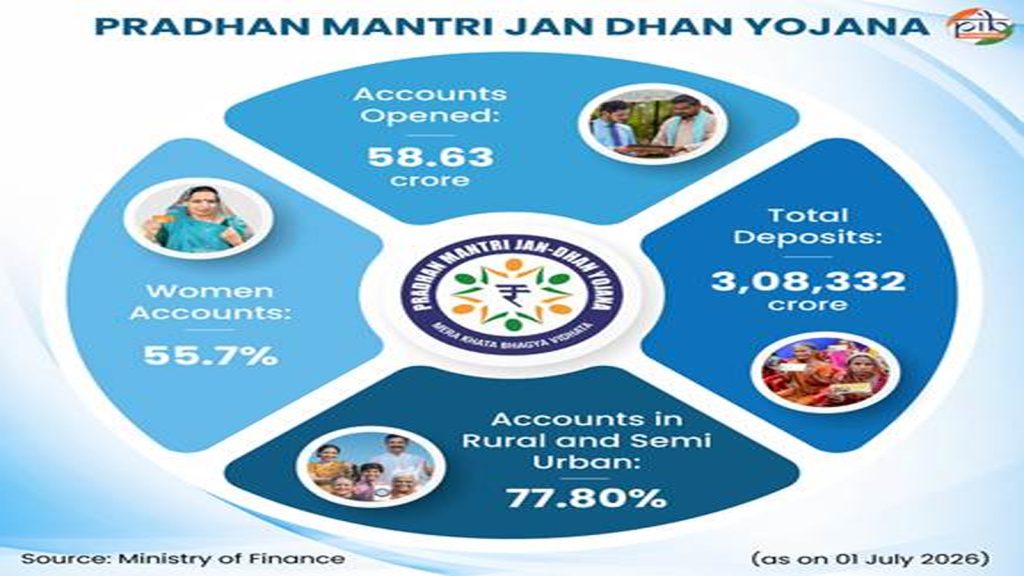

Financial inclusion has also expanded rapidly under the Pradhan Mantri Jan Dhan Yojana, which provides universal banking access along with credit, insurance and pension facilities while supporting Direct Benefit Transfers through the Jan Dhan-Aadhaar-Mobile (JAM) architecture. As of June 24, 2026, more than 58.63 crore Jan Dhan accounts had been opened with deposits exceeding ₹3 lakh crore. Women account for 32.68 crore of these accounts, while 45.62 crore accounts are located in rural and semi-urban areas.

The Jan Samarth Portal has emerged as a unified digital platform linking government-sponsored loan and subsidy schemes, including the Kisan Credit Card, enabling beneficiaries to identify suitable schemes and complete loan applications through a simplified digital process. Complementing these initiatives is the Jan Dhan Darshak App, which helps citizens locate banking facilities across the country while enabling the government to monitor financial access. As of March 6, 2025, 99.92 per cent of villages had a banking outlet within a five-kilometre radius, with Dadra and Nagar Haveli achieving complete banking coverage.

India’s rural credit system has steadily transitioned from an informal lending structure to a diversified, institution-led and technology-enabled financial ecosystem. Supported by strong institutions, targeted policy interventions and expanding digital infrastructure, the system is making formal finance more accessible across rural India. As institutional reach continues to deepen and financial inclusion expands, rural credit is expected to remain a critical driver of agricultural development, livelihood generation and inclusive economic growth.